Corporate executives call it “kitchen sinking.”

The minute you get into a new job you collect all the bad news, announce the miserable stuff at the same time and take the grisliest, most painful decisions all at once. You throw the kitchen sink at it.

You’ll have spotted this strategy before, and not just in politics – though George Osborne’s 2010 summer budget is often held up as the prime example.

Note how when a new chief executive takes over at a company, they will invariably begin by telling you the whole place needs a desperate clean-up and a change of strategy.

The autumn statement will be Rishi Sunak and Jeremy Hunt’s attempt to “kitchen sink” the bad news for the UK economy.

And to some extent, there’s little they have to do to amplify what’s already coming from the independent Office for Budget Responsibility (OBR).

The OBR’s forecasts for the economy – the official numbers against which the government must set its own policy decisions – were already shaping up to be pretty miserable long before Rishi Sunak came into Downing Street.

The UK is probably already in a recession.

It could be a long recession – though the many caveats to the Bank of England’s headline forecast for an eight-quarter long slump seem to have been forgotten in recent weeks.

What could the future hold?

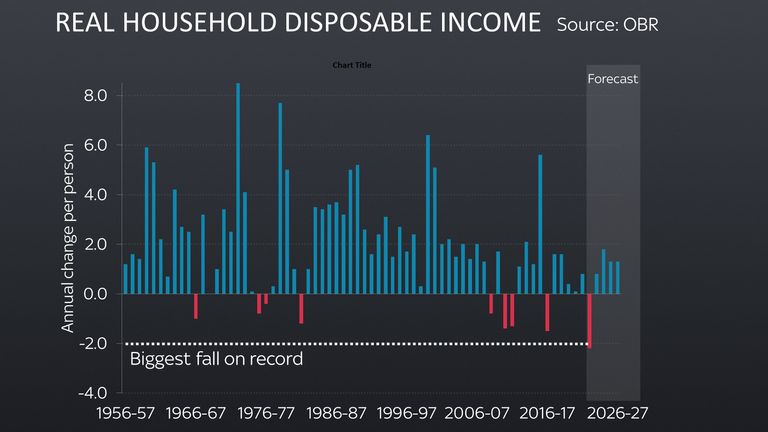

Either way, the news is not good, and this recession is likely to feel tougher than many others, in large part because this time it is not banks or businesses being squeezed but households themselves.

For evidence of this, look no further than the latest inflation data from the Office for National Statistics, which shows that housing and household service prices are rising at the fastest rate since comparable records began in the 1950s.

True: the path ahead is very uncertain.

If gas prices fall and the Ukraine conflict goes in the right direction, things could be a lot better than expected.

But trying to second-guess Vladimir Putin is a mug’s game. And in the meantime, the news is not good.

Britain, as a big importer of goods and for that matter energy, is very sensitive to increases in international prices, and we are going through an energy and price squeeze across much of the world.

And since our homegrown ability to generate income has not improved in the past year or so, those higher costs mean we are all, as a nation, worse off.

Britain is considerably poorer than it was last year – and this will be reflected in the OBR’s forecasts.

But the point of kitchen sinking is not merely to deliver all the bad news at once, but to announce some remedies – tough as they may be.

And that’s where the autumn statement really comes in.

What are we expecting from the autumn statement?

What was hitherto pitched by previous chancellor Kwasi Kwarteng as a brief update on the state of the public finances, and the government’s fiscal plan, has turned into something far bigger.

There will be spending cuts in real if not nominal terms and tax rises.

There will be warnings of a difficult couple of years to come.

And while Mr Hunt will emphasize that these “difficult decisions” will help provide the government with the room to cut taxes when the economy has recovered, the light at the end of the tunnel will feel quite distant.

There are a couple of reasons for this.

The first is that following the market mayhem of recent weeks, the Treasury wants to make abundantly clear to investors that it has a plan to repair the public finances. And it has a habit of overcompensating in moments like this.

One of the things that almost certainly unnerved investors back in September was that the mini-budget put the national debt on an ever-increasing trajectory.

The main task the chancellor is focusing on this time around is changing that trajectory so that the national debt is falling in five years’ time.

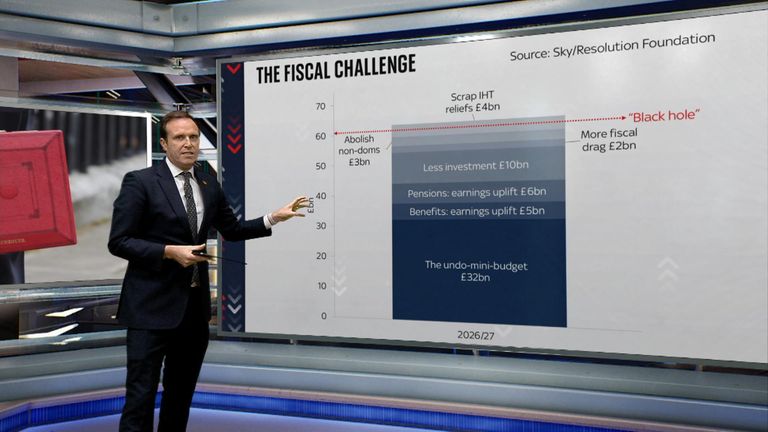

This is where the much-discussed “black hole” concept comes in.

What is the ‘black hole’ concept?

The “eye-watering black hole” the Treasury has talked about in recent weeks is actually something quite simple: the amount of spending cuts/tax rises it would take to get the national debt falling within five years.

That equates to roughly £50-60bn, once you take account of the stuff Jeremy Hunt has already reversed.

Now, these numbers are subject to enormous change, since they are based on imprecise estimates and the state of the economy is pretty unclear anyway.

But the gist here is that the Treasury is keen to over-compensate, much as it under-compensates in the mini-budget, sending a pretty clear signal to markets that it has a plan to reduce debt in the medium term.

And to meet that target, lots of bad news will be kitchen sinked: public sector pay settlements, departmental spending, tax rises for the wealthier, freezes in personal allowances.

Then there’s the energy price guarantee and what happens next year, namely a significantly scaled-back scheme to follow the £2,500 average price cap currently in place.

‘Black hole’ in finances explained

How could Tories reduce ‘£60bn black hole’?

Is Sunak’s goal unrealistic?

But the other reason Rishi Sunak wants to kitchen sink the bad news now is because he has another date in mind: 2024.

He believes that if the Conservatives have any chance of winning the next election, probably before the end of that year, they need to show both that they’ve repaired the mess of the past few months, and that the light at the end of the tunnel is no longer such a distant prospect.

His hope is that by raising taxes today, he’ll be able to promise to cut them (or even actually implement some cuts) by the election.

This might be an unrealistic prospect.

If the Bank of England’s forecasts are to be relied on, and that’s not a given, we may still be in the depths of a slump in a couple of years’ time.

Even so, Mr Sunak will be hoping he can replicate the path taken by another previous Tory administration, that of Margaret Thatcher.

She came into the office and, via Geoffrey Howe, delivered a heap of bad news in those first budgets.

Interest rates and taxes were raised.

It was the ultimate kitchen-sinking exercise but, so goes the Tory narrative, it laid the grounds for Nigel Lawson’s tax-cutting budgets of the late 1980s.

Click to subscribe to the Sophy Ridge on Sunday podcast

Others will argue today, as economists did back then, that it is madness to “tighten” fiscal policy even as the UK faces a recession and interest rates are on the way up.

Some will argue – with good reason – that there is little point in kitchen sinking some bad news without addressing the other stuff, like the fact that on top of everything else, Brexit is depressing trade growth and output.

Political strategists will point out that Thatcher might have lost her second election were it not for the Falklands War and the Labor Party’s lurch to the left.

More to the point, she could claim to be cleaning up the mess left by her political opponents; Rishi Sunak is cleaning up the mess left by his own colleagues from him.

Still, one thing is for sure: this will not be pleasant.